Investors have long argued that the price of gold is manipulated by central banks and their proxies. The basis for the argument is that gold is an international currency and often is considered a competitor to domestic currencies and sovereign bonds. A rising gold price usually signals weakness in the underlying currency and, by extension, the economy.

The theory is that Central Banks try to depress the price of gold to fend off competition for their domestic currencies. The organization GATA has even taken the US government to court over gold and silver price manipulation with other industry veterans testifying against hedge funds and investment banks in gold and silver manipulation cases.

The Organisation of Petroleum Exporting Countries (OPEC) sets quotas for the major national oil producers so that oil prices can be managed to maximise revenue. Too high and demand will fall and importing countries have a greater incentive to invest in research to find an alternative to oil. If the oil price is too low, then oil exporters are ceding revenue.

It stands to good reason that oil prices are supported by coordinated supply limits. If gold prices are suppressed to prevent them from rising, and oil is supported by OPEC, then if one was to measure the performance of gold and oil, they should see a marked divergence as the supported oil price rises against the capped gold price which will, in turn, reduce the return of gold bullion investments.

Many investors have decided that gold and silver manipulation has ruined the appeal of their investment and left them wanting to use any short-term spike in prices to sell gold coins and silver bars.

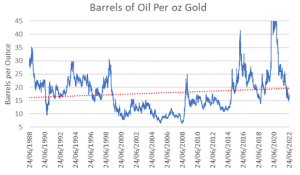

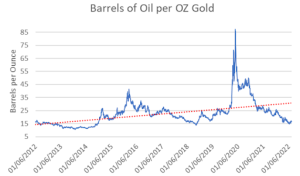

Review of data going back to 1988 was analysed so that a ratio was calculated to see how many barrels of Brent crude oil it took to buy an ounce of gold each day between June 1988 to June 2022. The result was that oil weakened slightly against gold as denoted by the red trend line on the following chart:

Even if the sample period is changed to remove the bull market of 2001, the result remains the same. A positive gradual trajectory can be seen over the past decade in which gold as gained against oil.

Does this mean that gold prices are not suppressed? No, but it fails to show any compelling evidence to support the notion that gold prices are contained. If gold is artificially suppressed, one would have expected to see a clear divergence of gold and oil prices with a distinct strengthening of oil relative to gold, but this is not the case.

It may be the case that the central banks have manipulated the gold price but not to the degree that some market participators believe. If gold or silver look to be breaking through a technical resistance, this will attract more buyers which predicts further gains. A central bank or proxy working on their behalf can aggressively sell into the market at technical resistances to prevent price breakouts.

It can do the same to force the market to break through a technical support to encourage further selling. This sort of manipulation is entirely plausible and will not show on the charts within this analysis.

Does this mean that gold bullion is just a bad investment?

Bullion prices have performed well and served the purpose of maintaining the investor’s purchasing power over time which fiat currencies have not done very well. A 2% inflation rate, which is a target for many of the developed nation’s central banks, infers that currency is being debased 2% annually. Gold and silver insulate investors from these as central banks can print bank notes, but they cannot print gold or silver bullion.

What is likely to be the main source of manipulation of gold and silver prices is the futures market. One can profit from the appreciation of the gold price without owning a grain of gold. This is done through unallocated gold contracts or through buying on the futures market.

If an individual wants to gain from a rising gold price, then there are some electronic/paper alternatives to physical gold which means that demand for gold is diluted, thus not influencing the physical market. A well-known phrase in the industry is “The futures markets are not manipulated; the futures markets are the manipulation”.

Based on market trends over the past few years, there are periods where retail demand for physical gold and silver increases and causes a disparity between the price at which physical bars and coins are trading at against the paper spot price. Should this disparity increase for a prolonged period, it could cause the spot price of both gold and silver to take-off with no central bank or proxy able to contain prices. So long as demand for physical bullion remains strong, it will become increasingly difficult for any financial entity to keep the gold and silver spot prices depressed. Investors should take advantage of this low paper price for bullion by buying physical.